|

| The Wiebe Family Budget Binder |

***************IMPORTANT NOTE**************************

Budgets don't work unless BOTH people in the relationship are involved. Seriously. If you don't both keep receipts, keep track of spending, and stay on the same page with what the goals are for your household, it just falls apart. Either one person gets exhausted with the up keep or one person spends money you didn't have or whatever just, people, PLEASE! Do your budget together. It is only an hour or so every couple weeks. THIS IS SO IMPORTANT! And you can count it as quality time?! Ok, it might be lame quality time; but necessary!

*DISCLAIMER*

I am not saying I am the most financially savvy person in the world and that if you follow these steps you'll be a millionaire. I have debt, the same as most people, and to be quite honest (and anyone who knows me will attest to this) I am terrible at math. However, we do our best to stay on top of the bills and budgeting. And so, our budget binder is very simple!

So here are the steps of how we budget and the things that are in our Budget Binder:

1. THE BILL CALENDAR

At the beginning of every month I fill in and print out our Bill Calendar. I use a simple calendar from Microsoft Publisher, and accent it however I feel suits the month. What goes on the calendar?

I put every single payment that will need to come out. Including a rough budget for groceries. I mark our paydays, and when our Child Tax Credits come in. (The link to find out what day you get paid is HERE ) I also mark any special occasions... Like Birthdays and Anniversaries, or Planned Long Distance Travel.

|

| A Mock-up of September's Calendar. |

The point of this calendar is an easy access to knowing what bills need to get paid from what paycheck. Payday morning, I sit down with the calendar and pay what bills need to be paid. I make sure there is enough money left in the account to cover automatic withdrawals, and a reasonable "float" for miscellaneous purchases, and gas. Then with what's left over- if there is any left over... sometimes there is not- I make payments towards our debt.

Interjecting here---> It is important to know what your main financial goal is. Ours right now is paying off our debt. A couple years ago, our main goal was saving for a house. In 10 years I'm sure our goals will be more focused on investing for retirement... It doesn't matter what you put your extra money to. the most important thing is to HAVE A GOAL! It makes deciding what to do with your money so much easier and tends to keep you from wasting your money on frivolous things *cough cough* takeout *cough cough*

2. RECORDING YOUR ACTUAL BUDGET:

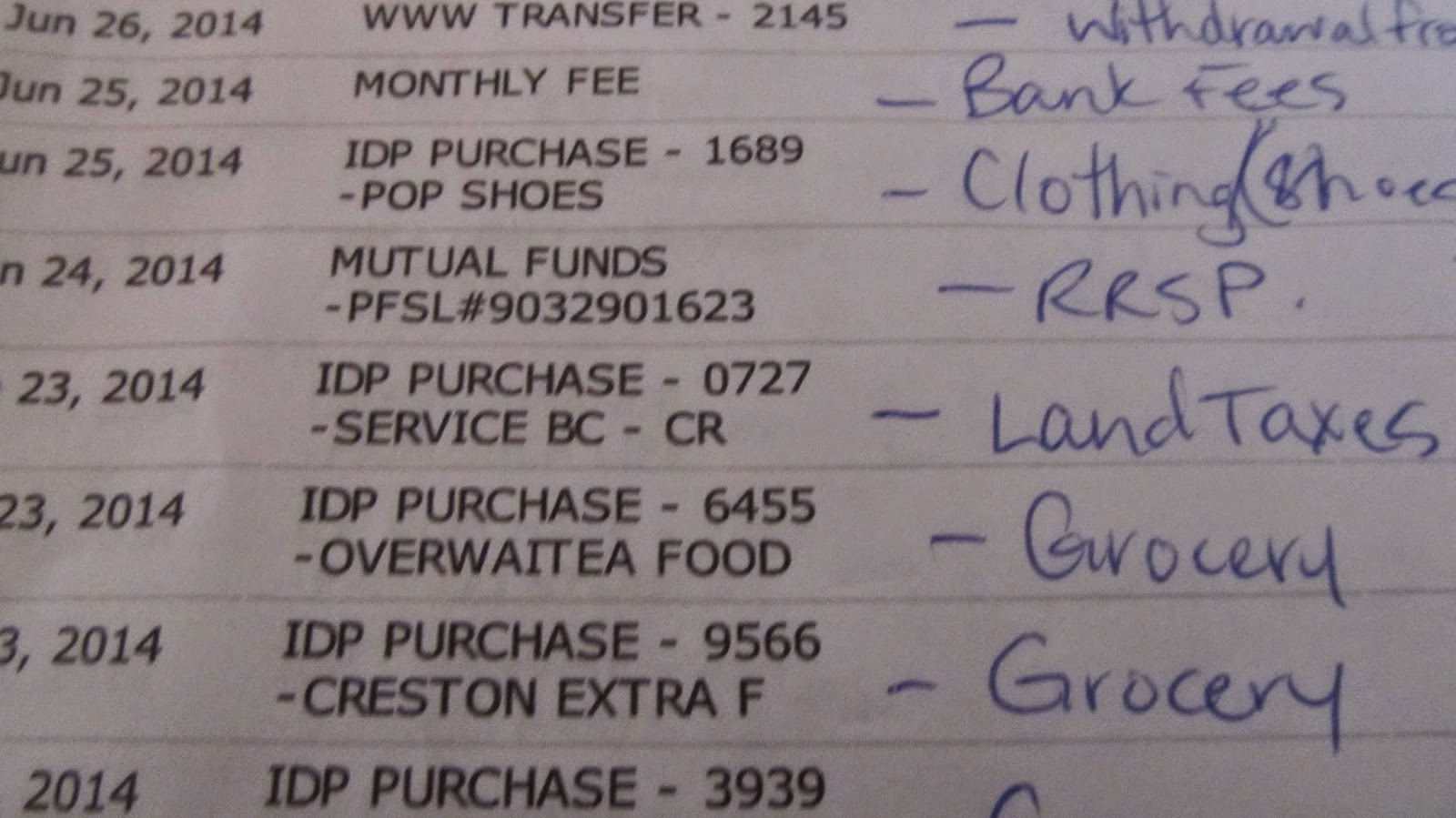

After paying what bills need to be paid I then print off the last two weeks of transactions from my online bank account. (Thankfully, mine has that option.)

I review the itemized list and assign each transaction to a group in my Microsoft Excel Spreadsheet Budget. Then I put the paper copy of the two weeks into the co-ordinating monthly tab in my binder.

I chose a simple family budget spreadsheet that adds your totals up and gives you a month by month trend report at the end of each line. It also keeps a YTD total at the bottom of each column (month) If Spreadsheets intimidate you... (like they did me) I suggest taking a tutorial of Microsoft Excel. That's what I did. It makes things A LOT easier to understand. Remember.... I am TERRIBLE at math. If you still feel nervous about a spreadsheet then you could just keep a total of your categories on paper. It was just too much work for me.

I would link a copy of my spreadsheet but not only am I terrible at math... I'm not that great with computers either! Hahaha. Seriously though, take a little tutorial online either through Miscrosoft Excel (what I did) or I'm sure you could YouTube it!

When itemizing your two weeks of spending/deposits I want to note that KEEPING YOUR RECEIPTS really helps! I have a plastic sleeve in my Budget Binder that I can throw receipts into so that every two weeks when I itemize my actual spent budget I know what was spent on what. Then I just throw out all the receipts to start the next two weeks (Unless, of course, there's something worth keeping for Taxes)

|

| The inside of my binder. Each month has the finished itemized list of credits/debits and there is a tab for Receipts and the Bill Calendar at the end. |

This is how we budget at the Wiebe Household. It's not very fancy... or complicated. But it works for us. How do you keep a budget?